The rate of change in wireless ecosystems is nothing less than fascinating.

I have been fascinated by Ray Kurzweil’s book “The Singularity is Near”for a while (great book, the documentary “Transcendent Man” gives a great summary, and apparently a movie is coming up too). Bottom line Kurzweil is charting the accelerating rate of technology change. That chart hits the x-axis in 2045 and that’s the singularity as it is unclear what happens then. Do we have to adapt? Are machines taking over?

While I am not sure whether we are all turning into pumpkins in 2045, or whether we will be able to adapt, the rate of change in wireless ecosystems is also nothing less than fascinating over the last decade. It may well be a good example of Kurzweil’s singularity – with the rate of change in the mobile ecosystem ever accelerating. The change of the associated landscape also neatly shows how software has completely changed the dynamic of system-level design. With the customer landscape changing so fast, even we allegedly sometimes socially challenged engineers have no good excuse not to meet new people.

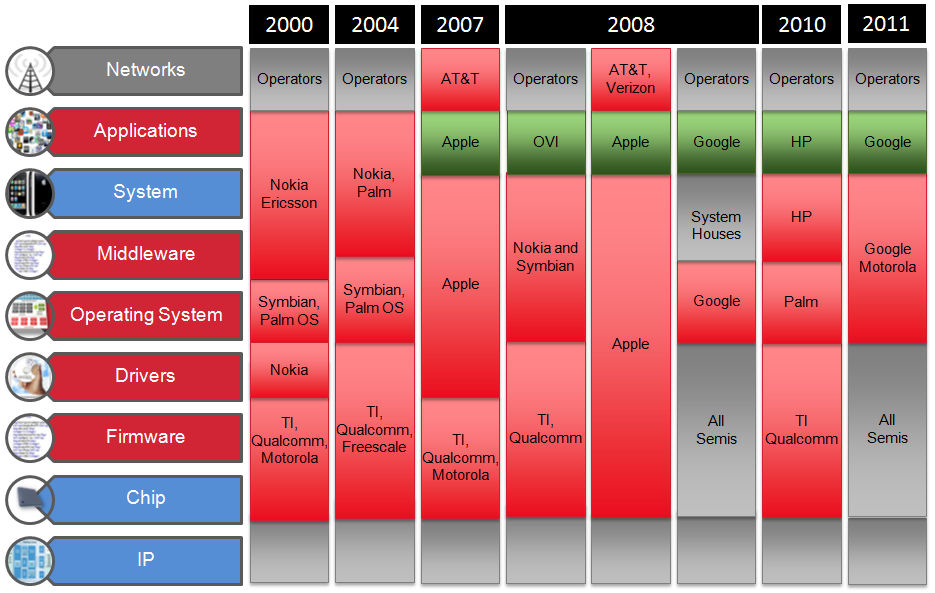

But let’s step back for a minute. The graphic in this post shows the dynamic of aggregation and disaggregation in the wireless communications industry. The value stack on the left shows the different components which need to be in place to develop mobile devices. Networks at the top are the interface to the end consumer. Apps running on systems – your smart phone, iPad or even your TV – are powered by middleware connecting the apps to operating systems, which by ways of drivers and firmware are mapped onto complex semiconductor chips and the semiconductor IP they assemble.

Aggregation and Disaggregation in the Wireless Communications Market

Once upon a time not too long ago, let’s say in 2001, there was a quite a bit of fragmentation. Semiconductor companies like TI, Qualcomm and Motorola were selling chips they had assembled from IP with added differentiation in hardware. The chips were sold to system houses like Nokia, Ericsson and Palm. These in turn would take the chips, use third party operating systems like Symbian, WinCE and PalmOS and deliver the devices to network operators.

Over time more and more differentiation went into software. Semiconductor companies could not sell the chips anymore without taking on more of the software. System houses increasingly specialized, spun out their semiconductor divisions – like Motorola spun out Freescale in 2004 – allowing system houses to differentiate more with what were the applications at the time. This went on for while. Responsibilities changed more and more, and in the design chain the suppliers were taking on more and more responsibility – typically in software.

In 2007 Apple came along, aggregated the operating system and hardware/software system development part with their iPhone and opened up the channel to differentiating applications. The industry was facing aggregation of the system portion and disaggregation of the software responsibility at the same time. From here things went on at an accelerating pace.

In 2008 Google had acquired what now has become Android, probably driven by the need to control more search in the growing mobile device market. Nokia reacted to both Apple’s iOS and Google’s Android by acquiring Symbian, representing further aggregation. Nokia initiated the OVI (not a three-letter-acronym but instead “door” in Finnish) app exchange, expanding it to Symbian. In parallel responsibilities of the suppliers continued to grow, and all the operating systems needed to be ported to the chip by the semiconductor vendor.

Also in 2008 Apple acquired PA Semi, a clear sign that hardware also does differentiate. With that move Apple took on much more of the semiconductor design and aggregated further, now owning almost the complete chain.

On the other side Google’s Android causes the complete opposite trend, disaggregation. Every system house could participate here building Android based systems, and so do semi suppliers who are powering Android with their chips. In 2010 others tried Apple’s aggregation as well – HP acquired Palm, struggling in number of applications on their OS. In parallel – not shown here – Nokia was orienting themselves upwards towards software and applications, and so was Research in Motion with their Blackberries, also aggregating more by acquiring OS provider QNX.

So where are we today? With the pending acquisition of Motorola by Google – we see aggregation again, do we? Bottom line, this market is fascinating, responsibilities change fast, software apps have completely disrupted the landscape. That’s why development practices for hardware/software systems need to reflect and enable those changes appropriately – the EDA360 vision is a good example, as are virtual prototypes, which in the past have been mostly used by semiconductor vendors but find their adoption in system companies at an increasing pace.

And looking at the speed of change here, this market is a great example of Kurzweil’s accelerating technology change. Hopefully we are not all turning into pumpkins in 2045 …

|

|

|

|

|

|

[…] than hardware developers, as I’ve tried to demonstrate in the past in previous posts like, “Putting Kurzweil’s Singularity to The Mobile Test.” As a result, EDA naturally has to expand to address the challenges its core customers […]

[…] DVD market, etc. I had myself in a previous blog post mused about acceleration of innovation in “Putting Kurzweil’s Singularity to the Mobile Test.” The acceleration of technology innovation that we are experiencing is nothing short of mind […]