Unit growth more than 13%, but selling prices are down and wafers are in short supply.

Semico Research is forecasting total semiconductor unit growth to exceed 13% this year, the first double-digit growth year since 2010. The exceptional unit growth is what the industry hopes for, but it does come with some growing pains.

MOS logic, optoelectronics, MEMS and sensors, and even analog and discrete products are experiencing more than 10% unit growth in 2017. The challenge is that ASPs (average selling prices) are taking a hit. For example, the MOS Logic ASP is expected to decline by 8%.

The growth in units is matched by a 9% growth in wafer demand. The increase in wafer demand would be even higher except that silicon wafers remain in a shortage situation and prices for silicon wafers are increasing. The price increase is impacting products that utilize both advanced and mature technologies. This is especially adverse for sensor products, which experienced double-digit ASP declines last year.

The effect of higher material costs already is being seen in the increased focus on yield improvements, more aggressive scaling transitions and other production efficiency enhancements. Mature processes for sensors and analog products such as biometric sensors, RF and power management continue to be in high demand, aided by growth in Internet of Things (IoT) and new mobile applications. Increasing silicon wafer prices are forcing manufacturers to improve productivity and to be more efficient with both 200mm and 300mm silicon wafers.

New products in the IoT category such as automotive, industrial and home automation will help boost semiconductor unit sales. Growth in the automotive sector—as well as industrial applications, including agriculture—is expected to expand as the semiconductor usage continues to increase.

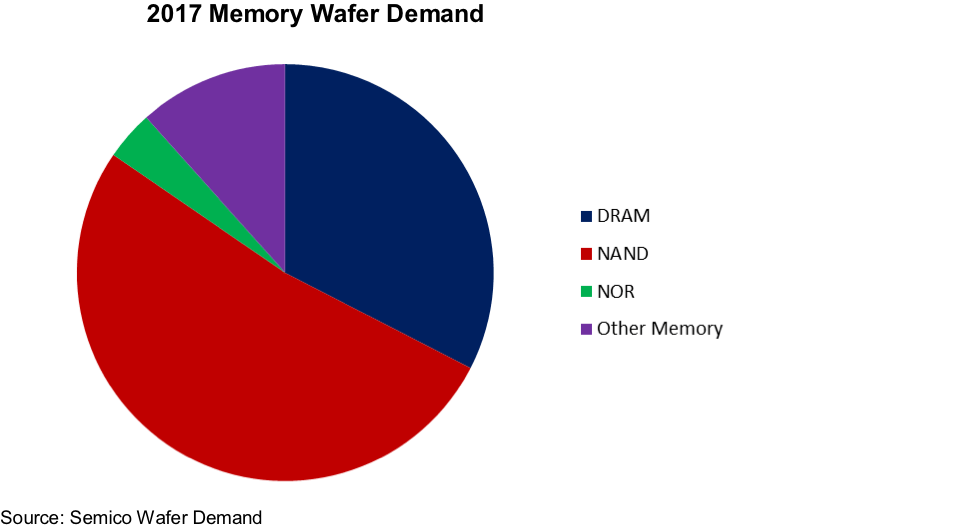

There is one market that is bucking the current trend. Memory unit growth is expected to be relatively flat at less than 1% growth, while ASPs will more than double.

Memory demand is increasing across all end applications, from mobile devices to servers to industrial and automotive. Combined with tight supply and rising wafer costs, memory manufacturers are aggressively transitioning to larger DRAM and NAND densities. This migration to larger densities allows manufacturers to supply the market with more memory bits per wafer. Not only does this strategy enable the suppliers to satisfy market requirements, but wafer demand for memory products is actually decreasing while memory ASPs are increasing. The net result is a more profitable situation for the memory suppliers. This higher profitability is funding new product R&D and future capacity expansion.

The higher than average unit growth is a welcome market trend this year, but Semico is forecasting only 4.3% unit growth in 2018. Keeping manufacturing costs down will require resourceful and unconventional solutions as material, equipment and process costs continue to rise and the market presses for lower ASPs.

Related Stories

Silicon Wafers: M&A, Price Hikes

Silicon wafer capacity is also tight.

200mm Crisis?

Demand is up, capacity is flat. A look at what’s behind this imbalance.

Will There Be Enough Silicon Wafers?

Market pressures shrink number of providers of basic building blocks for chips.

|

|

|

|

|

|

| |

|

|

Leave a Reply