Geopolitical concerns, economics and uncertain supplies are raising the anxiety level about availability across multiple supply chains.

Markets for critical metals are becoming turbulent, creating shortages and widespread supply chain concerns.

Critical metals are the raw elements and materials used in the production of aerospace/defense systems, automobiles, batteries, computers and electronic products. Many critical metals also are scarce, and there is high risk associated with their supply. In a recent report, the European Union (EU) lists 27 different raw metals/materials that are considered critical for systems and devices, including cobalt, gallium, germanium, graphite, hafnium, tantalum, tungsten and various rare earths.

Fig. 1: Critical raw materials for the European Union. Source: EU

The EU, the United States and others must import a large percentage of these raw metals/minerals from China, Congo and other nations. In 2016, for example, the U.S. was 100% dependent on foreign sources for 20 of the 90 metal/mineral commodities tracked by the U.S. Geological Survey (USGS). Of the 90, the U.S. must import more than 50% of 47 of those commodities, according to the USGS. (Other organizations have different lists for critical metals.)

The reliance of these commodities presents a range of supply chain issues that can affect specific products, broad markets, and in some cases spark national security concerns. Compounding the problem are rising product demand, geopolitical issues, mining disruptions and some unsavory business practices. Here are just some of the current issues in the market:

• Kobe Steel and Mitsubishi late last year separately disclosed that they falsified the strength and durability specs of certain finished copper alloys and other products. These products, which impact hundreds of customers, are used in aerospace, automotive, semiconductors, transportation and other industries. Kobe Steel and Mitsubishi have resolved some but not all issues.

• Prices for niobium, molybdenum, tantalum and tungsten are rising amid a tight supply for these metals.

• Rising demand for electric vehicles in China and elsewhere is expected to impact the supply of copper, cobalt, lithium and other metals.

• China still holds a monopoly of rare earths, which are used to make electronics products.

Not every metal/mineral is in crisis mode. Many are stable with an ample supply base. And some are at risk sometimes, but not others.

“Each one of them has supply chain issues that come up every once in a while,” said Lita Shon-Roy, president and chief executive of TECHCET, an advisory services firm that focuses on materials supply-chain issues for electronic devices. The firm tracks about a dozen different metal/material sectors. “The common stress point that comes up in most of these material areas has to do with raw materials and where they are coming from. The metal and mineral supply chain, for a long time, has been highly dependent on resources coming out of China.”

On top of that, demand is increasing for raw metals/minerals. Yet the mining industry generally has under-invested in new production for various reasons. “So there is a lot of pressure in the supply chain because of three elements—market growth, raw material dependencies, and a reluctance to add capacity,” Shon-Roy said. “On the business side, there are a lot of discussions with suppliers and end users to try and figure out how to minimize risk and ensure a continuous source of supply. From the supply side, they look on how to support this user without going broke.”

It’s impossible to explain the dynamics for all metals and materials. But the industry should keep closer tabs on the sector, especially cobalt, copper, lithium, tungsten, among others.

What are metals?

In the periodic table, 91 of the 118 elements are metals. The rest are non-metals or metalloids. Metals fall under different categories, including base metals (copper, iron, lead, nickel and zinc) and precious metals (gold, silver, platinum and palladium).

Several organizations have an arbitrary list of so-called critical metals and materials. Critical raw metals, according to the EU and others, are crucial to the economy and have risks associated with their supply.

At one time, the West wasn’t dependent on critical metals. In 1954, for example, the United States was reliant on foreign sources for 8 minerals, according to the USGS. But production of raw metals/minerals has been on the decline in the United States, due in part to costs and environmental issues associated with mining.

At the same time, huge metal deposits have been found in other countries, some of which have less stringent mining laws. For example, Chile has more than twice the copper reserves of any nation in the world. The U.S. imports 50% of its copper from Chile, according to the USGS.

Regardless, the use of raw metals/minerals is exploding. A computer went from using 12 elements in the 1980s to 60 by 2006, according to the National Research Council.

Today’s electronic products use a large percentage of all elements in the periodic table. “We see that demand for pure metals is a more significant driver than the supply. Consequently, we see strengthening in the pure metal market spaces,” said Greg Mlynar, director of marketing for semiconductors at Materion, a diversified supplier of materials and other products.

“Whether it’s in processing, graphics, portability, battery life, augmented/virtual reality, IoT, self-driving cars, robotics or MEMS, demand is increasing for pure metals like tungsten, copper and the precious metals,” Mlynar said. “Some of those applications are driven by things like the electrification of automobiles, EMI shielding for electronics and the use of copper in semiconductors. It crosses different material sets like copper, platinum and palladium. Those are materials used in applications like and various devices.”

Materials play a key role in the IC industry. For example, a leading-edge chip consists of three parts—the transistor, contacts and interconnects. The transistor resides on the bottom of the structure and serves as a switch. In the transistor, boron is used for p-doping, while phosphorous is used for n-doping. Future chips may use germanium in the channels.

The interconnects, which reside on the top of the transistor, consist of tiny copper wiring schemes that transfer electrical signals from one transistor to another.

A relativity new layer called the middle-of-line (MOL) connects the separate transistor and interconnect pieces using a series of tiny contact structures. The contacts are typically based on tungsten, but the structures are moving to cobalt at advanced nodes. “The requirements for performance and yield in the MOL metallization have made the replacement of tungsten by the low resistivity cobalt a necessity at the 7nm node and beyond,” said Nicolas Breil, director of technical projects at Applied Materials, in a recent presentation.

Fig. 2: Image of chip with front-end and backend. Source: Wikipedia

That’s just a small example of the materials mix in devices. New materials are also being used for memories such as . “You start out with an oxide/nitride alternating stack layer. Then, you wet etch the nitride layer out. Then, you backfill that with some sort of conductor. Right now, the industry standard is tungsten,” said David Hemker, senior vice president and technical fellow at Lam Research, at a recent event.

Copper woes

Each metal, meanwhile, has various dynamics. 2017 was a topsy-turvy year for copper, a metal with high thermal and electrical conductivity.

Worldwide production of mined copper fell by 3% in 2017, but it is expected to grow by 2.5% in 2018, according to the International Copper Study Group. In 2017, the decline was attributed to disruptions caused by a mining strike in Chile. But copper prices also reached a four-year high in 2017, thanks to demand from China, analysts said.

The big news in copper and other materials occurred late last year, when Kobe Steel found itself engulfed in a product quality scandal. The company revealed that it shipped various products with falsified specifications on the strength and durability of the metals.

The products in question are processed goods, such as aluminum flat-rolled products, aluminum extrusions, copper strips, copper tubes, sputtering target materials and others. These products are used in aircraft, automotive, flat-panel displays, machinery, semiconductors and others.

As it turns out, Kobe Steel delivered nonconforming products to 525 companies. So far, Kobe has certified the safety of the products at 505 companies. Kobe’s customers include Boeing, Ford, Toyota and others.

In December, Kobe Steel was stripped of several industrial quality certifications. Then, amid the Kobe Steel scandal, Mitsubishi late last year revealed it had shipped various products with falsified specifications. The products, which impact more than 200 customers, include brass and copper strip items, magnet wires and seals/O-rings.

Only a few companies have come forward and admitted that the faulty products from Kobe and Mitsubishi have impacted their systems. Many customers either declined to comment or insisted they have not been impacted.

It’s unclear if the issues have hit the semiconductor supply chain, but customers have expressed concern. “Yes, we have been concerned about the problems at Kobe; however, (the) expected impact on our business would be minor,” said Kenji Okuma, legal group manager for Mitsui High-tec, the world’s largest supplier of leadframes for IC packages. “As for Mitsubishi, we have been confirmed by Mitsubishi that all products delivered to us were not non-conforming products.”

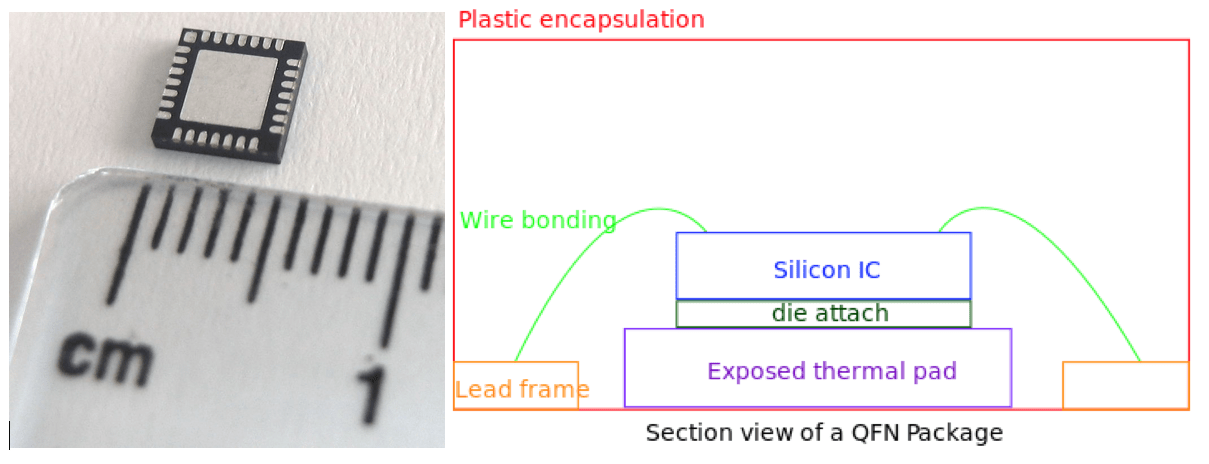

Leadframes are used for quad-flat no-lead (QFN) and other package types. A leadframe is a copper frame that consists of package leads and the frame. A die is attached to the frame.

Fig. 3: QFN package. Source: Wikipedia

Another leadframe supplier, ASM Pacific Technology, has also been assured by one of its copper suppliers that the delivered products met spec. “When we clarified with Mitsubishi, they claimed that all of the products we purchased from them are not affected,” said Stanley Tsui, group chief operating officer and executive vice president of ASM Pacific Technology, a supplier of equipment, leadframes and other products. Tsui is also chief executive of ASM Pacific Technology’s Material Business Segment group.

Leadframe suppliers have been impacted in other ways, however. In 2017, vendors were unable to secure enough copper alloy materials used to make leadframes for IC packages. Copper alloy suppliers diverted a large percentage of their production from leadframes for IC packages to high-margin connector products for automotive.

As a result of the copper supply issues, the lead times for leadframes increased to 10 to 12 weeks in 2017. Traditionally, lead times are three to four weeks. In 2018, meanwhile, long lead times are expected to persist for raw copper alloy materials for leadframes. But the leadframe products themselves are expected to move toward equilibrium.

Fig. 4: Leadframe examples (L-R), precision stamping, quality plating, photo etching. Source: Mitsui

More critical metals

The situation is not as dramatic for other metals, but there are some issues heading into 2018.

For example, H.C. Starck, a supplier of refractory metals, foresees higher raw material prices for 2018. “There have already been steep increases in raw material prices during the second half of 2017, especially for tantalum, niobium, molybdenum and tungsten,” said Andreas Mader, chief executive of the Fabricated Products Division at H.C. Starck, in a statement. “With the ongoing strong demand for these materials in the marketplace, it becomes vital that we ensure a continuous material supply of products to our customers. The current product price levels require upward adjustments and forward-looking discussions across our entire customer-base.”

Tungsten, for one, is used in the semiconductor and other industries. Tungsten fluoride or WF6, a compound of tungsten and fluorine, is used for depositing tungsten metal in devices.

“Tungsten supply/demand is in balance, but projections are expected to tighten over the next five years,” said Terry Francis, an analyst at TECHCET. “The growth in the demand for WF6 for 3D NAND keeps the gas suppliers working at near capacity.”

China provides 82% of the primary supply of tungsten with 95% of that supply controlled by one company, according to Francis in TECHCET’s “Critical Materials Reports on Sputter Targets and Metal Chemicals.”

Demand for other metals, such as cobalt, ruthenium, and tantalum, are expected to strain the supply chain in 2018, according to TECHCET.

Tantalum is one of the rarest elements on earth. In 2016, Africa supplied 63% of the world’s tantalum, according to Roskill, a market research firm. Demand for tantalum is expected to grow by 3.3% between 2017 and 2026, the firm said.

Capacitors remain the largest market for this material, but the growth is slowing. The faster growing applications include sputtering targets, chemicals and mill products, according to the firm.

Prices of tantalum depend on the status of the mines. If there is an oversupply, mining companies tend to “shut the mine down when there is too much slack and availability,” TECHCET’s Shon-Roy said.

Electric car boom

Today’s electronic products require a slew of materials. But one technology—electric vehicles—is projected to require an enormous amount of raw metals, possibly turning the supply chain upside down.

In total, carmakers are expected to ship 91 million new vehicles in 2020, according to CRU, a research firm. Of those, carmakers are projected to ship 2.1 million new electric vehicles, or 2% of the world’s car market, in 2020. By 2030, carmakers are expected to ship 107 million vehicles, CRU said. Of that, the industry is projected to ship 31.7 million electric vehicles, or 30% of the world’s market, by 2030.

China alone seeks to put 5 million electric vehicles on the road by 2020, requiring a 40% increase in new-energy-vehicle sales each year, according to McKinsey & Co.

All of these figures might be optimistic. But if the industry does indeed ship 31.7 million electric cars by 2030, the industry would require 4.1 megatons (Mt), or 4.1 million tons, of copper, according to mining giant Glencore. The figures include the requirements for cars and the infrastructure.

Fig. 5: Global copper demand for EVs. Source: CRU

“That’s around 18% of today’s supply (of copper),” said Ivan Glasenberg, chief executive of Glencore, in a recent presentation. “So the world will need a large amount of copper just for electric vehicles. That is ignoring the other growth in demand for copper.”

By 2030, the electric car industry will also require 1.1Mt of nickel and 314Kt of cobalt, according to Glencore. To meet the demand for cobalt, the industry needs to triple the amount of cobalt supply by the year 2030, Glasenberg said.

Fig. 6: Demand for metals for electric vehicles. Source: Glencore

There are several key parts to electric vehicles, including the battery and infrastructure. A battery consists of an anode (negative), cathode (positive), electrolytes and a separator. In a simple operation, ions are transported from the anode to the cathode and back.

Electric vehicles use lithium-ion batteries. Graphite is used for the anode. The cathode is based on lithium with other metals. For example, Tesla uses a battery based on lithium with a nickel cobalt aluminum (NCA) mix.

The supply of cobalt is a concern. Cobalt, a by-product of copper and nickel, is largely mined in the Democratic Republic of the Congo (DRC). In addition, China refined 54% of the world’s cobalt in 2016, and also produces 80% of the world’s cobalt chemicals, the form that appears in lithium-ion batteries, according to Benchmark Mineral Intelligence, a research firm.

“The demand side (for cobalt) is strong due to lithium-ion battery growth and in high-performance alloys, tool materials and catalysts,” TECHCET’s Francis said. “It is on the conflict material list and both Intel and Apple have strong restrictions on any use of cobalt from the DRC. Pricing has risen dramatically and is expected to be volatile over the next three years.”

Amid the demand for electric and hybrid cars, automotive OEMs are scrambling for cobalt. “Currently, the cobalt market is very tight in terms of supply and demand,” said Caspar Rawles, an analyst at Benchmark Mineral Intelligence. “The issue will arise in the future as the growth rate of demand will outstrip the speed at which the supply chain can respond. This is why we have seen the prices rise over the last 12 months.”

In 2016, the worldwide supply of cobalt was 93,000 tons, according to Benchmark. Last year, the demand for cobalt from just the lithium-ion battery industry alone was 48,000 tons, according to the firm.

By 2021, the lithium-ion battery industry will require 78,000 tons of cobalt. The figure includes all lithium-ion batteries, such as EVs, hybrids, and portable electronics.

Going forward, the industry hopes to reduce its reliance on the DRC for cobalt. “There will be no lithium-ion battery industry without DRC cobalt, and it will play the biggest part in responding to the increase in cobalt demand,” Rawles said. “Having said this, there is also a need for supply to come online that reduces the dependency on the DRC for cobalt. There is some scope for increasing supply in some existing projects, including some of the larger nickel projects in Indonesia and the Philippines. Also, exploration and development outside of the DRC have focused on Canada and Australia, where we expect some additional supply to come from.”

Cobalt isn’t the only problem. “In the near term, lithium is one of the key minerals where a lack of supply could hinder the speed at which lithium-ion cells, and ultimately EVs, can be produced,” Rawles said.

“Looking toward the future, as cathode technology develops, we are moving towards higher nickel/lower cobalt formulations,” he added. “As this happens and the industry grows, there could potentially be a shortage of battery-grade nickel chemical. The nickel industry is far larger than cobalt or lithium, so the concerns of oversupply are still some way off. But as the industry grows, this will be one to follow closely.”

There are other changes. “In terms of raw (cobalt) material, the largest producer in the world is Glencore, who produced around 28,000 tons in 2016. When we talk about the battery industry, largely material from the DRC is shipped to China to be refined to battery chemicals or precursors. These are then distributed the battery/cell manufacturers, the largest of these being CATL, BYD, Samsung and LG Chem,” he said. “Cobalt refiners/cathode manufacturers or cell manufacturers purchase materials directly and sell finished cells to the auto manufacturers. But we think this is likely to change in the future and we will see more vertical integration involving the auto manufacturers. This has already happened in the lithium market, when Great Wall made a deal with Pilbara Minerals. This was an important moment as it was the first time an auto manufacturer was directly involved with a miner for an off take of raw materials.”

Related Stories

New BEOL/MOL Breakthroughs?

Different materials, approaches for contacts and interconnects begin to surface for 7/5nm.

The Race To 10/7nm

Next nodes are expected to be long-lasting, because costs of developing chip after that will skyrocket.

Many Paths To Hafnium Oxide

What makes a good precursor in atomic layer deposition isn’t clear.

Materials For Future Electronics

Flexible electronics, new memory types, and neuromorphic computing dominate research.

|

|

|

|

|

|

| |

|

|

Leave a Reply