The country is banking on DRAM and NAND to reduce its trade deficit.

China’s fledging memory makers are expected to reach a major milestone and move into initial production this year, although vendors are already running into various roadblocks.

China’s domestic vendors are focusing on two markets, 3D NAND and DRAM. In both cases local vendors are either behind in technology, struggling to develop these products, or both. And one vendor recently was hit with a lawsuit over alleged trade theft, renewing fears about the lack of intellectual-property (IP) protection in China.

Still, China is moving full speed ahead in memory as well as IC design, logic and packaging. Armed with billions of dollars in funding, China wants to develop its domestic semiconductor industry because it currently imports the vast majority of its chips from foreign suppliers. That has created an enormous trade gap.

In logic, China has made a tiny dent in the trade gap over the years. And China recently announced several major projects to shrink that gap. Among them:

It’s unclear if China can get a foothold in the market. Local vendors have some IP, but they are basically starting from scratch. To help propel its efforts, the nation has attempted to acquire multinational memory makers or form alliances. Most have balked, citing national security and IP concerns.

So China must develop most of the technology itself. But it’s difficult to play catch-up in the competitive memory market against the multinationals such as Intel, Micron, Samsung, SK Hynix, Toshiba and Western Digital.

That raises questions about whether China’s memory makers will succeed in the long run. Some analysts are pessimistic, saying that the domestic vendors lack competitive technology. Others are slightly more upbeat about China’s domestic memory efforts.

“We are a bit more optimistic on NAND than we are in DRAM, but it’s going to take some time,” said Handel Jones, chief executive of International Business Strategies (IBS), a market research firm. “(China has the) ability to gain share in NAND, but you still need leadership technology. But for a new DRAM company to come in and gain access to technology, it will be very tough.”

China is roughly six to nine months away from developing a 64-layer 3D NAND device, a technology that could put the nation on the map, according to multiple sources. Volume shipments are still anywhere from one to two years away, so it remains to be seen if China can make reliable parts, sources said.

Others have a different viewpoint on the market. “Semico believes the success of three Chinese-owned memory companies is highly unlikely, but the success of a single Chinese memory company is very probable,” said Joanne Itow, managing director of manufacturing at Semico Research, in a recent blog.

In total, the capacity among China’s domestic memory vendors is projected to increase from nearly zero today to more than 300,000 wafers per month (wpm) by 2021, according to Semico. This may sound impressive, but it will represent less than 10% of the worldwide memory capacity by then, according to Semico.

Ambitious plans

Over the years, China has unveiled several initiatives to advance its domestic IC industry. It has made some progress, although every plan has fallen short of expectations for several reasons. For one thing, China was late in modernizing its IC industry. Then, for years, the United States and other nations imposed strict export control regulations for China, which prevented multinational equipment vendors from shipping the latest gear into China. Recently, though, many export controls have been relaxed in in China.

Still, China found itself in a troubling situation. It became an enormous manufacturing base for electronics products, but the nation could produce only a small fraction of its own chips.

In 2012, China consumed $82 billion, or 32%, of the world’s chips, according to IC Insights. But IC production in China was $8.8 billion in 2012, which represented only 10.8% of the world’s production of semiconductors, according to IC Insights. So, China imported about 90% of its chips.

Seeking to reverse those trends, the Chinese government unveiled a new plan in 2014, dubbed the “National Guideline for Development of the IC Industry.” The plan was designed to accelerate China’s efforts in 14nm finFETs, advanced packaging and memory.

China also created a $19.3 billion fund, which would be used to invest in its domestic IC firms. Local municipalities and private equity firms also pledged to spend $100 billion across China’s IC sector.

Then, in 2015, China launched another initiative, dubbed “Made in China 2025.” As part of the effort, China hoped to increase its domestic IC production from less than 20% in 2015, to 40% in 2020, and 70% by 2025, according to IC Insights.

China’s efforts have produced mixed results. A number of new fabs have appeared in China, but it must still import a huge percentage of chips.

In 2017, China consumed $138 billion, or 38%, of the world’s chips, according to IC Insights. IC production in China reached $18.5 billion in 2017, equating to 13.3% of the world’s production, according to the firm. “This is the number that drives the Chinese government crazy. They look at this metric and say this number needs to be bigger,” said Bill McClean, president of IC Insights.

So, China will likely fall short of its self-sufficiency targets for chips in 2020 and 2025, according to McClean, although the nation continues to move forward with its ambitious plans.

In total, the nation is currently building 19 new fabs, with 10 of those projects being 300mm plants, according to SEMI analysts Dan Tracy and Clark Tseng. The numbers include both domestic and multinational chipmakers.

It’s unclear if all these fab projects will get off the ground, because the dynamics in China remain fluid. Regardless, equipment vendors are gearing up for the start of a fab tool spending spree in China.

Year-end equipment forecast. Source: SEMI

“We expect wafer fab equipment investment in China being up in 2018 by about $2 billion compared to 2017,” said Arthur Sherman, vice president of marketing and business development at Applied Materials. “And from what we’re seeing, we believe that investment will grow over the next several years-incrementally higher going forward.”

Memory lane

China’s domestic IC foundry vendors are viable players today, producing a sizable number of chips for local and multinational customers. TSMC and UMC also have fabs in China, while GlobalFoundries is building one as well.

Then, the nation’s memory business is divided into two categories-multinationals and domestic players. In 2006, SK Hynix was one of the early multinationals to build a DRAM fab in China. Intel and Samsung produce 3D NAND in China. Today, though, the total output from those fabs represents a tiny fraction of the overall demand in China.

China’s reliance on foreign sources for memory has created some supply chain issues. Last year, DRAM prices spiked, creating cost pressures for smartphone OEMs, including those in China. In response, the Chinese government recently intervened and asked Samsung to moderate the price increases for mobile DRAM in the first quarter of 2018, according to TrendForce, a research firm.

That’s just a short-term fix for a larger problem, though, which is why China is trying to get a domestic memory industry off the ground. “China semiconductor market demand and the China government’s strategic emphasis on the semiconductor industry have fueled the recent rapid growth of new domestic players in China,” said Brian Trafas, executive vice president of the Global Customer Organization at KLA-Tencor.

Needless to say, China’s memory players face several challenges. “The new domestic players will need to focus on R&D progress, attracting and developing key talent, and successfully ramping new fabs,” Trafas said. “A few unique challenges in ramping in China are the geographically spread-out customer base and the shortage of experienced talent.”

China’s most notable efforts in memory started in 2006, with the emergence of Wuhan Xinxin Semiconductor Manufacturing Corp. (XMC). Wuhan-based XMC is a NOR flash foundry vendor. In addition, XMC has been developing 3D NAND as part of an alliance with Spansion, now part of Cypress.

In 2016, Tsinghua Unigroup acquired a majority stake in XMC. Then, XMC was moved under a new group called Yangtze River Storage Technology (YRST).

Tsinghua Unigroup and its memory unit, YRST, have announced three major memory projects in China in recent times. Here is the latest activity:

Recently, Tsinghua Unigroup has set up a firm to invest in the Chinese city of Chongqing, according to reports. It’s unclear if the firm will invest in memory, however.

On the memory front, Tsinghua Unigroup broke ground on the Nanjing fab in late 2017, but there has been little activity since then. And in Chengdu, the company hasn’t announced a timetable for the fab.

China’s big hope centers around YRST’s efforts in Wuhan. For some time, YRST has been developing 3D NAND within XMC’s fab. Last year, YRST broke ground on a new fab in Wuhan, near XMC. This fab is almost completed with plans to produce 5,000 wpm by mid-2018, according to IC Insights. E-mail inquiries to YRST’s executives were not returned.

Regardless, YRST faces a steep learning curve, as 3D NAND is more difficult to make than previously thought. Even the multinational vendors struggled in 3D NAND, as the technology requires a number of new and difficult steps in the fab.

NAND flash memory itself is used for solid-state storage drives and smartphones. Until recently, planar NAND was the prevailing technology. Planar NAND is still viable, but it’s reaching its physical limit at the current 1xnm node regime.

3D NAND is the successor to planar NAND. Unlike planar NAND, which is a 2D structure, 3D NAND resembles a skyscraper, in which horizontal layers are stacked and then connected using tiny vertical channels.

3D NAND consist of multiple layers. Samsung’s latest 3D NAND device is a 64-layer, 3-bit-per-cell device. So the device has 64 layers stacked on top of each other, enabling a 256Gb product. The bit density increases with the number of layers.

YRST is sampling a 32-layer 3D NAND part, but 32- or 48-layer devices are no longer competitive from a price-per-bit standpoint. So YRST’s goal is to accelerate the development of its 64-layer technology, which is in R&D, sources said. The 64-layer product is targeted for production in the new Wuhan fab, but the line may start with the 32-layer chip. That’s because the 64-layer technology is still not ready due to yield issues, sources said.

For China, the 64-layer device is critical. A 64-layer 3D NAND device is price competitive and will remain the sweet spot for some time. “64-layer technology will be a long-term technology node in 3D NAND,” IBS’ Jones said. “It’s the same way as 28nm is for logic.”

In China, there is less urgency to migrate to the next iteration-96-layer 3D NAND technology. The cost-per-bit benefit is less dramatic here. “When you go to 96 layers, the cost reduction is maybe 10% to 15%. When you go to 128 layers, it’s may be another 5%,” Jones said.

Still, the multinational suppliers that are ramping up 64-layer devices are also developing 96-layer 3D NAND parts. To be sure, the multinationals have the know-how to advance 3D NAND.

YRST has some know-how and IP, but it faces some challenges moving from 32 to 64 layers. “64-layer technology is very tough,” Jones said, “but we think they will get the technology.”

3D NAND is difficult because it relies on an assortment of new deposition and etch steps. Suppliers can buy the equipment on the open market, but the development of 3D NAND requires know-how. “The tooling that you can get from Applied and Lam is very good,” he said. “But you still have to operate it to develop device structures.”

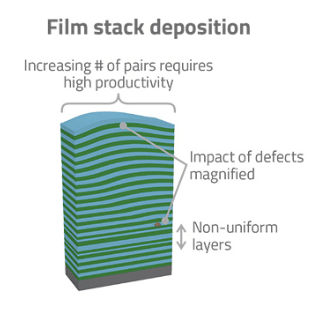

In the 3D NAND flow, for example, alternating films are stacked on a substrate using deposition. The process is repeated several times. But as more layers are added, the challenge is to stack the layers uniformly and without defects.

Film stack deposition challenges. Source: Lam Research.

In the next step, a plasma etcher then etches tiny circular holes or channels from the top of the device stack to the bottom substrate. Each channel must be uniform. Otherwise, CD variations may occur.

Channel etch challenges. Source: Lam Research

There are other steps involved, but the key issue is yield. “As yield is the critical deciding factor for the success of these China semiconductor companies, process control has been significantly emphasized (in China),” KLA-Tencor’s Trafas said.

DRAM hopefuls

Meanwhile, China also wants to be a DRAM player, but this is a mature and competitive market. At the high end, Samsung is ramping up 18nm DRAMs.

As a starting point, though, China’s DRAM makers are developing 22nm parts. “The technology is not going to be near the leading edge,” IC Insights’ McClean said. “There is a market for it, but it’s pretty thin.”

China could gain some traction in DRAM. The government could enforce a mandate under which Chinese OEMs must incorporate a certain percentage of local DRAM in their systems. “If you make the Chinese electronic system producers use less-than-competitive memory technology, you are going to put them at a disadvantage in the market,” McClean said.

Unfazed by the odds, China’s Innotron is readying its first product-22nm mobile DRAMs. Located in Hefei, the capital of the Anhui province in eastern China, Innotron is a joint venture between GigaDevice and the Hefei City Government.

Innotron will move the equipment into a new 300mm fab in the first quarter of 2018, according to IC Insights. The total investment in the fab will reach $7.2 billion with a total capacity of 125,000 wpm, according to IC Insights.

Many expected Innotron to obtain some technology from GigaDevice, a fabless supplier of flash memories. Some time ago, GigaDevice announced plans to acquire specialty DRAM maker Integrated Silicon Solution Inc. (ISSI). ISSI is owned by Uphill Investment, a Chinese consortium of investors.

But last year, the GigaDevice-ISSI deal was terminated, according to a spokesman from GigaDevice. This in turn raises questions where Innotron will obtain its technology. The GigaDevice spokesman declined to comment on the progress of Innotron.

Meanwhile, in 2016, JHICC broke ground on a 300mm fab in Jinjiang City in the Fujian province in southern China, at a cost of $5.65 billion. JHICC’s investors include Fujian Electronics & Information and Jinjiang Energy Investment.

In Q3, JHICC plans to move into production with 22nm specialty DRAMs. It obtained the technology from a licensing/R&D alliance with UMC. UMC isn’t involved with JHICC’s operations.

JHICC has run into some legal issues, though. In December, Micron filed a suit against JHICC and UMC for alleged theft of Micron’s technology, according to the suit. Then, in January, UMC filed a counter claim against Micron, alleging that Micron infringed upon UMC’s patents. The litigation is still ongoing.

IP issues are just one of the challenges. China’s memory makers also face stiff competition in a tough market. “I look at this at maybe almost like what China did in the foundry industry. They have 10% market share. Maybe China will get 10% of the memory market,” IC Insights’ McClean said. “I don’t think it would be zero. But I don’t see big chunks of market share coming out of Samsung, Micron and Hynix anytime soon.”

Related Stories

China Unveils Memory Plans

China: Fab Boom or Bust?

China’s Ambitious Automotive Plans

NAND Market Hits Speed Bump

|

|

|

|

|

|

|  |

China’s neighbors (Taiwan and South Korea) could pull it off (chip making) in less than two decades. They too had little know-how when they had started their journey but now leading the industry. So it appears to be a matter of time.

Thank you for this great article and the inspiration.

An advanced metrolog is a key for successful characterization for promising yield.

China isn’t in it for the money, at least not for the first 5 years. So they could afford to sell it at cost. That is assuming their cost ( Yield ) could be competitive.

And other thing is China has been paying huge sum of money to bring experts into their field from Samsung, TSMC, UMC, Micron or others. And I expect that to work out well, although how fast they could being those knowledge into Real world remains to be seen.

I was hoping we see effect of NAND prices by mid 2018, but judging from the rather slow start of Fabs. May be they are a little cautious.

If it wasn’t due to lower Smartphone demand, 128Gb MLC NAND prices have stay the same for nearly 3 years. And unless China can act, I am pretty sure all the NAND and DRAM makers have agreed they will milk the market for as long as possible to prepare for China’s attack.

Very good article with great insights!

There are multiple challenges to both 3D NAND and DRAM players in China. However, China will make it!

Taiwan and South Korea could do it from scratch, China can easily do it with the market size and financial capital.